|

The Drowning Middle Class In One ChartChris MenahanInformationLiberation Feb. 24, 2020 |

Popular

US and Iran Agree to Two-Week Ceasefire

Trump Threatens Iran With Genocide If They Won't Meet His Demands: 'A Whole Civilization Will Die Tonight'

Trump Says U.S. Sent 'A Lot of Guns' to Iranian 'Protesters'

Trump Expected to Pick Kevin Warsh, Son-in-Law of Zionist Billionaire Ron Lauder, as Fed Chair

Reuters: Trump Approved Iran Strikes After Speaking With Netanyahu

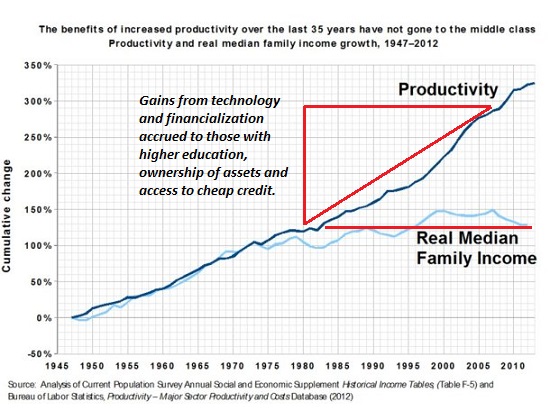

Americans over the past 35 years have had their effective incomes dramatically eroded due to the surging costs of college, health insurance, housing and transportation, according to a new study from the Manhattan Institute. Americans over the past 35 years have had their effective incomes dramatically eroded due to the surging costs of college, health insurance, housing and transportation, according to a new study from the Manhattan Institute. From The Manhattan Institute, "The Cost-of-Thriving Index: Reevaluating the Prosperity of the American Family" (via The Washington Post): A dramatic divergence between data and experience is confounding America’s policy debates. The data seem to show that households have attained unprecedented prosperity, and wages have (at worst) held their own against inflation, or (at best) risen much faster than prices. By conventional measures, material living standards everywhere in the income distribution are at all-time highs, and technological progress continues to improve them. Yet many jobs able to support a family in the past no longer do. Millennials are in worse financial shape than were those of Generation X at the same age, who themselves had fallen behind the baby boomers. The stories appear irreconcilable.Contrary to what our ruling oligarchs tell us, it's not just in our heads that a man today has to work two jobs to make as much as his father made 30 years ago (on top of being systematically discriminated against). "Popular perception is correct," lead author Oren Cass said on Twitter. "In 1985, the typical male worker could cover a family of four's major expenditures (housing, health care, transportation, education) on 30 weeks of salary. By 2018 it took 53 weeks. Which is a problem, there being 52 weeks in a year."  More from the Manhattan Institute: Products that spread risk offer everyone value in formal economic terms, but only those who suffer the risky outcome receive a tangible benefit. If health-insurance premiums rise because conditions present in 1% of families can now be treated with new and extremely expensive procedures, prices have not increased for inflation purposes. But 99 out of every 100 households that have to pay more for their insurance will never experience any perceptible change in the quality or quantity of their health care. Good analyses of economic well-being are usually careful to focus on outcomes at the median, rather than the mean; yet when it comes to the asserted improvement in material living standards associated with higher health-care spending, the gains are present only on average and are concentrated in a very small fraction of the distribution.  This is why a lot of Trump's rhetoric (and Obama's in the past) seems to fall flat when he boasts about how strong our economy is. Though the stock market is way up, around 45 percent of Americans don't own any stocks and the richest 1% reportedly own 50% of the stocks held by American households. Our economy seems to have shifted into a kleptocratic looting operation with the end of Bretton Woods in 1971 when Nixon ditched the gold standard. Our ruling oligarchs have been swimming in cheap money ever since while the middle class has been drowning due to inflation.    There's no doubt mass immigration on top of suppressing wages has also played a huge part in the rising costs of college, health insurance, housing and transportation:  Follow InformationLiberation on Twitter, Facebook, Gab and Minds. |